$85,000 to $100,000. That is the current estimated cost per year to pay for long-term care.

Don’t think you’ll need it? Think again. There is a 70% chance that someone turning 65 today will need some type of long-term care. Those numbers will go up, as people live longer each year. Those care needs may be in the home or a senior living community.

While these numbers can be intimidating, there are options available right now to prepare you for your long-term care needs.

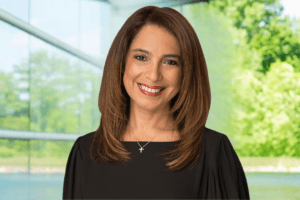

A Place At Home recently sat down with Matthew Hooker, a financial advisor with Edward Jones. He shared there’s not a specific age to start planning for long-term care. “I’ve seen people do it as early as 40-45. Because they have seen it, and they are willing to pay to avoid it.” He advises if you start early, then you can address it before it’s an issue. And that’s the best assurance you can get. In the past, long-term care policies were a use it or lose it proposition. It was incredibly expensive to carry a plan, and the rates would go up. Often when people transitioned to a fixed income.

Fortunately, that’s not the case these days. According to Matthew, now there are great options for long-term care policies.

Some of these are hybrid policies, encompassing coverage for both assisted living situations as well as life insurance. He explained some of the options available to help you prepare for your long-term care needs:

- Integrate long-term care into your budget (self-insuring): This allows you the most flexibility in choosing your care providers, but paying out of pocket for long-term care can be costly and can be a gamble for your financial goals.

- Long-term care insurance – If you choose to go through an insurance company, you have a couple of options:

- Traditional long-term care insurance:

- Policies and costs vary quite a bit, based on different things, such as your health, age, location of care, and more. It can ensure you won’t deplete your assets and income if you need long-term care. It also offers flexibility and possible shared benefits between two people. However, premiums are not fixed or guaranteed. You do still have to pay them, even if you don’t need care later.

- Life insurance with long-term care benefits: these policies are newer and can allow you to use the death benefit to pay for long-term care if you need to. Premiums here are generally fixed, and if no care is required, it provides a life insurance death benefit. There are additional costs with these hybrid policies, and the long-term care coverage is often less than with a traditional long-term care policy.

Saving for your potential long-term care needs can be like a roulette wheel. How you decide to plan for your future depends on your individual needs.

Matthew advises that whatever you decide to do to prepare for long-term care as you age, make sure you have a game plan that makes sense. “I take people’s priorities, their picture of retirement, and give them different vehicles to get to where they want to go.” He also shares that a large part of his role is interpreting what people’s needs really are. “Long term care, assisted living, nursing home care, people use all these words interchangeably, and none of them mean the same thing.” Matthew knows the difference between all of these, as well as the ever-changing rules and regulations, changes in legislation, and especially long-term care and assisted living. Everyone’s situation and goals are different. “I work with people and interpret whoever they are as a person.”

“Their experience? That experience is what you have to get down to, and really understand.”

Matthew will help you plan for how you envision your future. He does comprehensive planning, including full-blown insurance and investments, stocks, bonds, mutual funds, 401k’s, cash accounts, money markets, refinancing your home (which he does not recommend), estate planning, and trusts. Helping people is something Matthew has a passion for. He shares, “I truly love this profession, this job. I get paid for it, thank God because I would do this anyway. I love helping folks.”

Whatever your current situation or future goals are, A Place At Home recommends speaking with Matthew to ensure your needs are met. And to ensure you are set up for any potential long-term care needs you may have in the years to come. You can reach him by visiting his website, sending him an email, or calling him at 402-630-7379. With all the uncertainty, especially with what we’ve seen this year, reaching out to Matthew might be one of the best things you can do to prepare for your future.

Need guidance looking for in-home care, or choosing an assisted living community? Reach out to us today to explore your options!